You come home after a stormy day to find your refrigerator humming oddly, your TV won’t turn on, and your HVAC system is fried. After the initial panic fades, one question starts racing through your mind: does homeowners insurance cover electrical surge damage?

Many assume their homeowners insurance automatically covers electrical surge damage, but that’s not always the case — and the details matter more than most people realize.

In this article, we’ll break down exactly when and how insurance might cover electrical surges, what steps you must take to prove a power surge to your insurer, and why documenting damage properly can make or break your claim.

What Is Electrical Surge Damage?

An electrical surge, often referred to as a power surge, occurs when there is a sudden spike in electrical current flowing through your home’s wiring. These spikes can damage or destroy any device plugged into your system, including TVs, computers, kitchen appliances, HVAC systems, routers, and more.

Power surges can result from:

- Power grid switching by your utility provider

- Downed power lines

- Faulty wiring or damaged transformers

- Large appliances cycling on/off (like refrigerators or AC units)

This kind of damage can be devastating — not just financially, but emotionally, especially when sentimental or high-cost devices are affected.

Does Homeowners Insurance Cover Electrical Surge Damage

The short answer is: sometimes — but not always.

Most standard homeowners insurance policies do include coverage for sudden and accidental damage, which may encompass electrical surge damage, particularly if caused by a covered peril like lightning. However, insurance companies may deny or limit coverage if the surge originated from a power grid issue, faulty wiring, or the policyholder’s own electrical system.

Here’s a breakdown of how different causes are typically handled:

Cause of Surge | Usually Covered? |

Lightning strike | ✅ Yes, under most policies |

Utility company power grid issue | 🚫 Not always — may require special endorsements |

Internal electrical failure | 🚫 Usually excluded |

Appliance malfunction | 🚫 Usually excluded |

Surge protection system failure | 🚫 Often excluded or limited |

In Bucks and Montgomery County, many homes are older or experience frequent storm-related outages. That’s why it’s important to have surge-related clauses reviewed carefully — or request policy upgrades that extend coverage.

If you’re unsure whether your policy includes electrical surge damage insurance, it’s worth speaking to a public adjuster or your insurance rep before disaster strikes.

How to Prove Power Surge to Insurance

If your property suffers a surge, documentation is key. Insurers often require extensive evidence before approving any payout for electrical damage.

Here are practical steps you should take:

- Check Your Devices Immediately

Make a list of every appliance, system, or electronic item that has stopped working properly after the surge. Include brand, model, and estimated age. - Get a Licensed Electrician’s Report

A licensed technician can inspect the damage and provide a report verifying that a surge caused the failure. This is often the most important evidence. - Keep Damaged Items

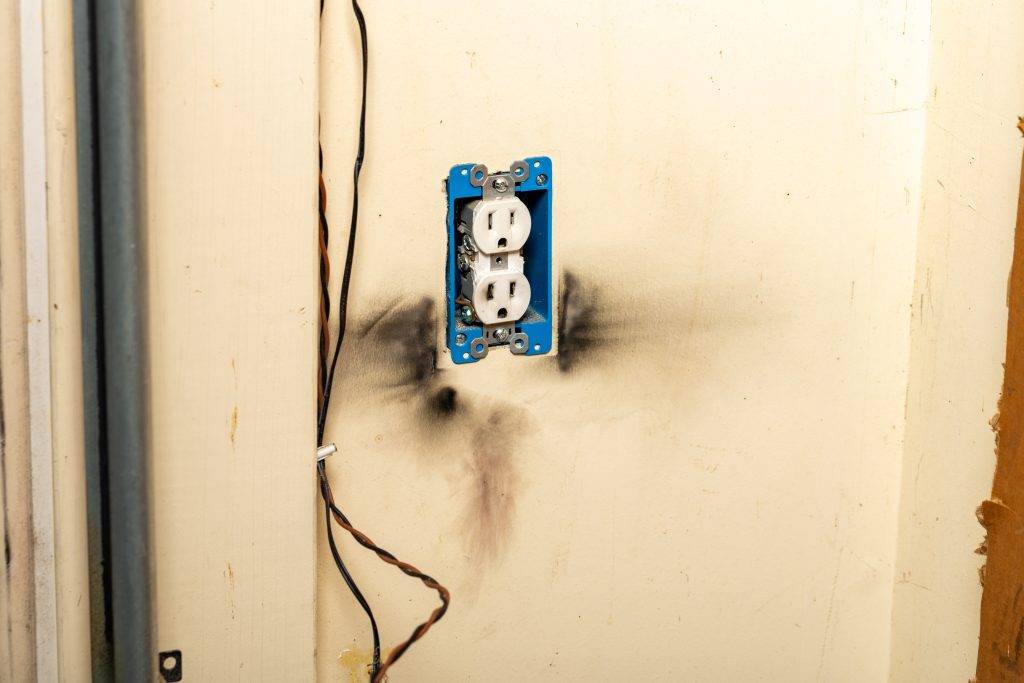

Do not dispose of any damaged electronics or appliances before an adjuster inspects them — they may be needed for verification. - Take Photos and Videos

Document any physical signs of damage, such as scorched outlets, melted cords, or burnt circuit boards. - Request a Power Company Report (if applicable)

If the surge came from your local utility (common in Doylestown, Lansdale, or Norristown), request written documentation of any outages or surges in your area. - File Promptly

File the claim as soon as possible, and be honest in your claim description — misrepresentation can lead to denials.

Electrical Surge Damage Insurance: Common Mistakes to Avoid

Even if electrical surge damage insurance is part of your policy, many claims are denied due to technicalities or lack of evidence.

Avoid these common mistakes:

- Assuming all surge damage is covered – Policies often exclude damage caused by internal wiring issues or homeowner negligence.

- Not having whole-home surge protection – Some policies require surge protectors to be in place to validate claims.

- Waiting too long to report – Delays in filing can trigger suspicion or loss of evidence.

- Filing a claim without expert help – Many homeowners unintentionally undervalue their loss or fail to document properly.

A licensed public adjuster, like our team at Alliance Adjustment Group, can help you sidestep these issues and deal with the insurer on your behalf.

How a Public Adjuster Helps With Surge Claims

Public adjusters represent you, not your insurance company. Our job is to:

- Review your policy for applicable surge damage coverage

- Collect and organize proper documentation

- Bring in expert inspectors and electricians

- Negotiate a fair settlement on your behalf

- Appeal denied or underpaid claims

Unlike the insurance company’s adjuster, we’re on your side — and we work on a contingency basis, so there’s no upfront cost to you.

Need Help With a Power Surge Insurance Claim?

If you’re in Bucks County, Montgomery County, or anywhere across Pennsylvania and you’ve experienced electrical surge damage, don’t go through the claims process alone. Contact Alliance Adjustment Group today.

Disclaimer:

The information provided on this website is for general informational purposes only and does not constitute legal advice.

While we strive to provide accurate and up-to-date information, insurance policies and regulations can vary. It is important to consult with your specific insurance provider or a qualified professional for advice tailored to your individual circumstances.